Why prepared contractors are moving before the market becomes obvious

Infrastructure demand is still moving across Australia, but opportunity is increasingly emerging through staged procurement, enabling works and contractor panels rather than all at once.

For operators, that means fleet readiness, utilisation and finance structure are becoming more important before demand accelerates — not after pressure appears.

Table of Contents

- Infrastructure Demand Is Still Moving

- The Market Is Changing — Not Slowing

- Why Staged Procurement Changes the Game

- HumeLink, Transmission Infrastructure & Early Capability Positioning

- Precinct Infrastructure Is Creating Secondary Demand

- Prepared Contractors Often Move Earlier

- Productivity Pressure Is Changing Competitive Advantage

- Why Readiness Is Becoming Commercially Valuable

- Final Thought

- FAQs

One of the biggest misconceptions in construction and infrastructure markets is that opportunity arrives all at once.

In reality, demand often moves quietly first.

Before the headlines.

Before wider urgency.

Before the broader market reacts.

And increasingly across Australia’s infrastructure pipeline, projects are now progressing through delivery models that reward:

- Preparedness

- Capability

- Utilisation

- Operational readiness

That shift matters, because in many cases, the businesses best positioned for future work are not reacting once demand becomes obvious.

They are positioning before it accelerates.

Infrastructure Demand Is Still Moving

As explored in TMF’s June Infrastructure Update: Positioning Before Demand Accelerates, billions of dollars of infrastructure investment continue progressing across:

- Transmission infrastructure

- Utilities upgrades

- Precinct development

- Regional civil infrastructure

- Enabling works

Projects including:

- HumeLink

- Marinus Link

- Western Sydney Aerotropolis

- Bruce Highway upgrades

continue signalling long-term contractor demand across:

- Excavation

- Trenching

- Compaction

- Drainage

- Haulage

- Enabling civil works

- Utility infrastructure

Importantly, many of these projects are not being delivered through traditional “single start date” construction environments.

They are increasingly progressing through:

- Staged procurement

- Contractor panels

- Enabling packages

- Early Contractor Involvement (ECI)

- Progressive delivery environments

That changes how opportunity emerges.

The Market Is Changing — Not Slowing

There is still significant discussion across the market around:

- Interest rates

- Operating costs

- Labour shortages

- Productivity pressure

- Construction volatility

Those pressures are real.

But many operators are mistaking changing delivery conditions for disappearing opportunity.

They are not the same thing.

In reality, many infrastructure programs are still progressing — just differently.

Projects increasingly involve:

- Enabling works first

- Staged contractor engagement

- Progressive mobilisation

- Long-duration delivery models

That means demand often begins moving before wider market confidence fully returns.

Why Staged Procurement Changes the Game

Across infrastructure and major project delivery, staged procurement and Early Contractor Involvement (ECI) models are becoming increasingly common.

Infrastructure Australia has highlighted increasing use of collaborative procurement and ECI models across major infrastructure delivery.

Infrastructure NSW procurement guidance also references increasing use of early contractor involvement strategies on major projects.

These delivery environments often reward businesses that:

- Prepare earlier

- Demonstrate capability earlier

- Maintain operational readiness

- Preserve mobilisation flexibility

- Maintain reliable fleet utilisation

Because by the time wider demand becomes obvious, many early opportunities may already be moving.

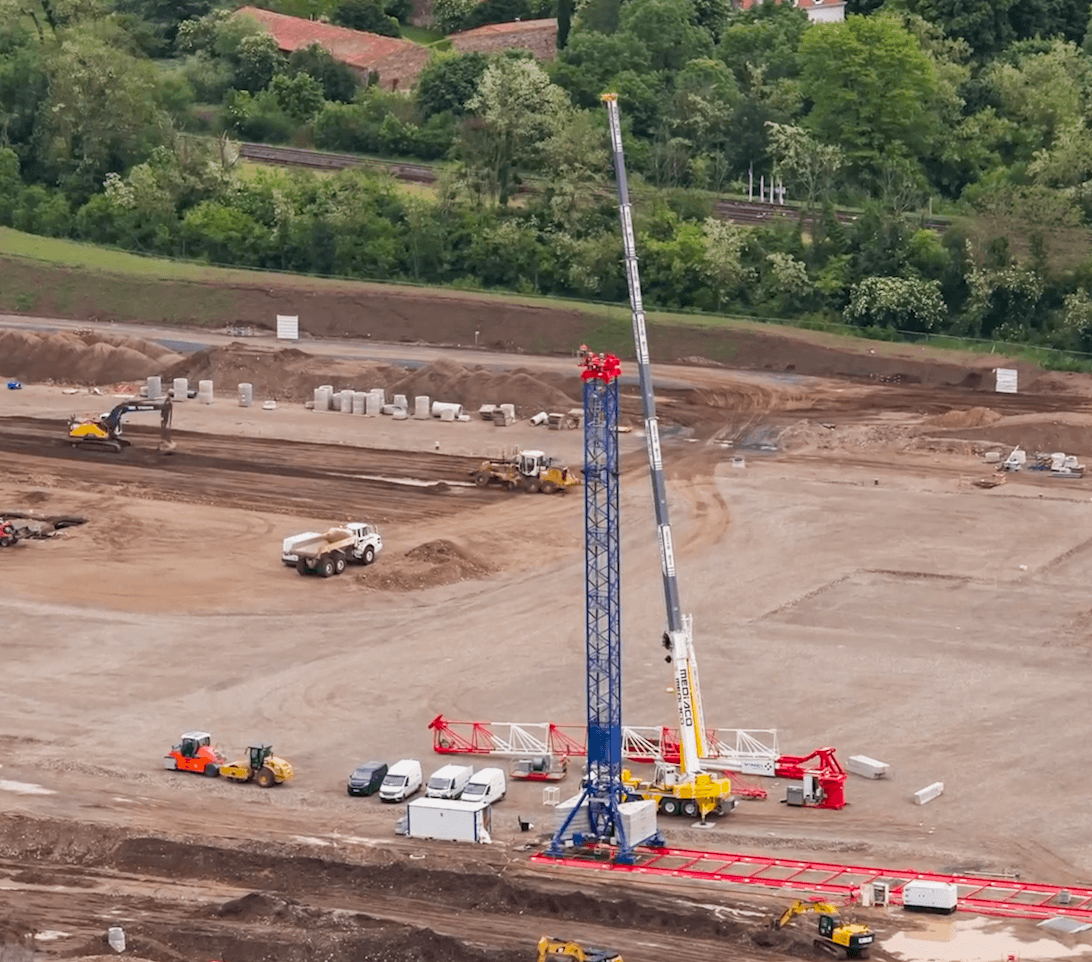

HumeLink, Transmission Infrastructure & Early Capability Positioning

One of the clearest examples of this shift is HumeLink.

Transgrid describes HumeLink as one of New South Wales’ largest energy infrastructure projects, involving approximately 365 kilometres of new transmission infrastructure.

Projects of this scale create demand across:

- Trenching

- Corridor preparation

- Utility infrastructure

- Access roads

- Enabling civil works

- Support fleet

Importantly, projects like HumeLink progress progressively over multiple years.

HumeLink West construction updates confirm major construction and enabling works are now underway.

That matters because transmission infrastructure often rewards:

- Delivery capability

- Uptime

- Mobilisation readiness

- Operational consistency

before wider market urgency fully appears.

Precinct Infrastructure Is Creating Secondary Demand

The same pattern is emerging across large precinct ecosystems like Western Sydney Aerotropolis.

Many operators focus only on the headline project.

But major precinct ecosystems often create years of secondary contractor demand through:

- Utilities

- Drainage

- Enabling works

- Supporting road infrastructure

- Staged civil delivery

And these environments often favour operators that:

- Remain flexible

- Maintain strong utilisation

- Preserve working capital

- Prepare fleet capability earlier

rather than businesses trying to react once demand peaks.

Prepared Contractors Often Move Earlier

The strongest operators are rarely making decisions based only on what the market looks like today.

They are increasingly asking:

- What will demand look like in 12–24 months?

- What capability gaps exist now?

- What equipment creates stronger utilisation?

- What creates operational flexibility?

- What improves delivery confidence?

That is a very different mindset.

Because prepared contractors understand that momentum often compounds earlier than urgency.

Productivity Pressure Is Changing Competitive Advantage

This shift is happening while Australia’s construction sector continues facing productivity pressure.

CEDA construction productivity research notes that construction productivity has remained weak for decades while delivery complexity continues increasing.

CEDA analysis also found larger construction firms generate significantly higher revenue per worker than smaller operators due to:

- Scale

- Technology adoption

- Operational efficiency

- Delivery capability

At the same time:

- Labour shortages remain challenging

- Project complexity is increasing

- Timelines remain pressured

- Delivery expectations are rising

That means productivity and utilisation are becoming increasingly important commercial differentiators.

The strongest operators are increasingly focused on:

- Uptime

- Readiness

- Delivery capability

- Utilisation efficiency

- Operational certainty

—not simply fleet size.

Why Readiness Is Becoming Commercially Valuable

In changing markets, readiness itself is becoming commercially valuable.

Because when opportunities emerge through:

- Staged procurement

- Contractor panels

- Enabling works

- Transmission infrastructure

- Utilities delivery

The businesses best positioned are often the ones that:

- Prepared earlier

- Reviewed fleet earlier

- Preserved flexibility earlier

- Improved utilisation earlier

- Positioned before urgency appeared

That edge matters.

Especially in environments where projects increasingly reward capability before demand becomes obvious.

Final Thought

The market is not standing still.

Infrastructure demand is still moving across:

- Transmission

- Utilities

- Precinct development

- Regional civil infrastructure

But the way opportunity emerges is changing.

This cycle is increasingly rewarding:

- Preparedness

- Delivery capability

- Operational readiness

- Utilisation

- Flexibility

before urgency appears.

Because in many cases, the businesses that move strongest later are the ones that positioned earlier.

Talk to TMF

If you’re reviewing fleet capability, preparing for future infrastructure demand or assessing how to position the business more confidently for the next 12–24 months, TMF can help you map out your options clearly.

Book an obligation-free planning call with TMF and start positioning early — or assess your finance readiness and estimate repayments.

Related Reading

If ageing equipment, downtime or rising repair costs are starting to affect your fleet performance, read: The Cost of Delay: Why Ageing Equipment Can Quietly Drain Margin.

For the broader market context behind this article, read: TMF June Industry Update: Positioning Before Demand Accelerates.

FAQs

Why are infrastructure opportunities appearing earlier in the cycle?

Many projects are now progressing through staged procurement, enabling works and contractor panel environments rather than traditional “all-at-once” delivery models.

That means capability positioning often begins before wider market demand becomes obvious.

What is Early Contractor Involvement (ECI)?

Early Contractor Involvement is a procurement model where contractors are engaged earlier in the planning and delivery process to improve:

- Constructability

- Risk management

- Delivery efficiency

- Project coordination

ECI models are becoming increasingly common across major infrastructure projects.

Why does readiness matter more in 2026?

Projects across transmission infrastructure, utilities and civil construction increasingly reward businesses that maintain:

- Reliable fleet capability

- Strong utilisation

- Mobilisation readiness

- Delivery consistency

before urgency appears.

Why are transmission infrastructure projects important?

Projects like HumeLink and Marinus Link represent billions of dollars of long-term infrastructure investment and create practical contractor demand across:

- Trenching

- Excavation

- Utility infrastructure

- Enabling civil works

- Support fleet

These projects often progress progressively over multiple years.

What are prepared contractors doing differently?

Prepared operators are increasingly:

- Reviewing fleet earlier

- Improving utilisation

- Preserving flexibility

- Assessing funding capacity

- Positioning capability before demand accelerates

rather than reacting once pressure appears.

How can finance structure help operators prepare earlier?

The right finance structure can help businesses:

- Preserve working capital

- Align repayments to utilisation

- Improve flexibility

- Maintain operational readiness

- Position for future opportunities more confidently